Private Equity Real Estate Funds Chasing Smaller Deals & Portfolios

Author:

Managing Director

Over two-thirds of private equity real estate funds are finding it harder and harder to hunt down attractive real estate acquisitions than 12 months ago, according to a recent report by Preqin, an industry-leader in alternative assets and real estate fund data provider.

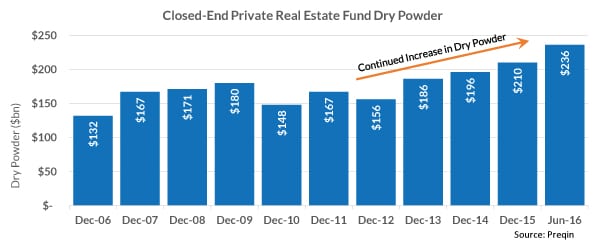

Lots of Dry Powder in Private Equity Real Estate Funds

As such, the amount of undeployed capital is now at an all-time high, reaching $236 billion this month. This is an increase of $16 billion or 7.6% over December of 2015, continuing the trend since the most recent low in December 2012 with a total of $80 billion and 51% over the 3-1/2 year span.

Private Real Estate Funds Competing Against Institutions

Private real estate fund managers are also competing against highly capable institutional real estate investors who are showing increased willingness to commit capital directly to real estate investments rather than employ fund strategies.

In order to effectively deploy capital, fund managers are using creative strategies to find areas where there is less competition:

- Buying Portfolios – Portfolio acquisitions are substantially more complex, which scares away funds who lack the ability to perform sophisticated real estate investment analysis and underwriting on a large number of properties. Portfolio underwriting aside, once under contract, these transactions have a lot of moving parts and an enormous amount of due diligence to dig through in what often ends up being a fairly short closing timeframe.

- Buying Smaller Deals – Smaller deals require less sophistication, but because of their size, real estate funds that employ this strategy must close on a substantially larger number of them to deploy the same amount of capital. These individual acquisitions aren’t nearly as complicated, but the due diligence can still be challenging because the books and records provided by the sellers tend to be in more disarray. Also, the sheer volume of potential acquisitions a fund manager must review can be daunting, which means the review and underwriting process must be streamlined to ensure the best deals don’t get overlooked.

- Specialized Assets – Even though specialized assets like Student Housing, Self-Storage, and Seniors Housing make up only 3% of the overall transactions, this is a 200% increase over 2015. Firms eager to deploy capital are looking to non-traditional real estate sectors to find opportunities that meet their return criteria.

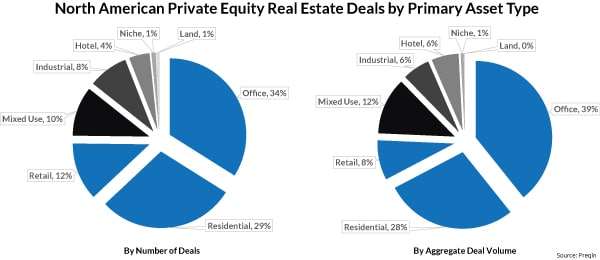

Private Equity Real Estate Fund Asset Allocation

In North America, the “Big 3” asset types continue to be Office, Residential and Retail, making up 75% of the number of deals and 76% of the aggregate deal value.

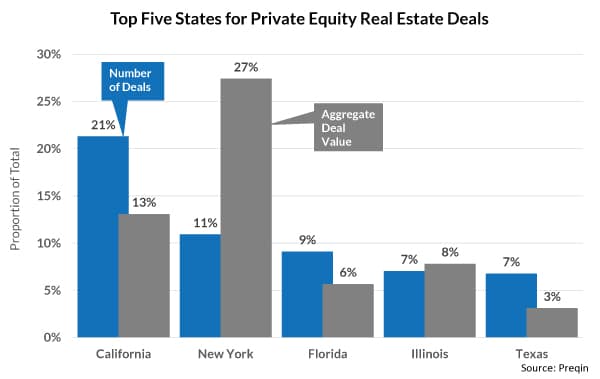

In the United States, private equity real estate funds targeted California for more deals than any other state, however New York held the top spot by aggregate deal value. Other states in the top 5 were Florida, Illinois and Texas.

Sources:

Link to the Report: https://www.preqin.com/docs/reports/Preqin-Special-Report-Real-Estate-Deals-June-2016.pdf

Link to the Data: https://www.preqin.com/REDEALS16

Other Coverage: